Investment Zones are a lot like Freeport tax sites, arguably with more benefits, so are they friend or foe to Freeports?

Background

Liz Truss pledged to boost growth with “full-fat” Freeports as part of her leadership campaign in July 2022 and it sounded like all systems were finally go for Freeports. The creation of Freeports was first introduced as part of the Conservative party’s general election manifesto in 2019, but it was then slow to get started with the locations of the first eight Freeports not being announced until March 2021.

Then, last month, Chancellor Kwasi Kwarteng announced in his ‘mini-budget’ that the government is talking to 38 local authorities in England about new plans for Investment Zones. Comparisons were immediately drawn to those previous announcements and pledges in respect of Freeports. Investment Zones are a lot like Freeport tax sites, arguably with more benefits, so are they friend or foe to Freeports?

How do Investment Zones compare to Freeports?

The designation of land within a Freeport can be split into two types; customs sites and tax sites.

A customs site is a secure area offering with the potential for:

- Customs Deferral: deferring the point at which customs declarations must be made to provide either a cashflow benefit where finished goods are released into the UK market, or disapplying the requirement for a customs declaration where finished goods are exported.

- Tariff Inversion: a reduction in liability where the duty payable on finished goods is less than the duty payable on the separate components or raw materials making up the finished goods.

Although similar benefits can be obtained under different customs procedures, customs sites within Freeports can be advantageous to businesses, with simplified record keeping requirements, and much of the administrative responsibility shouldered by the customs site operator. Customs sites remain exclusive to Freeports.

However, a tax site within a Freeport would appear to be the model on which Investment Zones are being built. Both sites offer full stamp duty land tax (SDLT) relief, enhanced capital allowances, enhanced structures and buildings allowances, employment tax incentives, and business rates relief. The table below provides an ‘at a glance’ comparison of Freeport tax site and Investment Zone benefits.

The reference by the Prime Minister to “full-fat Freeports” appears to be centred around the benefits associated with Investment Zones; namely:

- longer lasting reliefs (potentially up to 10 years),

- higher relief for enhanced structures and buildings allowances,

- employer NICs relief applying up to a higher salary threshold, and

- SDLT relief available in respect of land and buildings purchased for residential development.

Are Investment Zones going to enhance Freeport sites or draw investment away?

There is some concern that Investment Zones could merely redistribute existing economic activity. That point was considered by the Adam Smith Institute in a report published on 21 September 2022 entitled “Seeing it Through: A Plan for Full-Fat Freeports”, by Sam Ashworth-Hayes:

“Some redistribution of economic activity through strategically situated freeports would fit with the government’s Levelling Up agenda. But if freeports did no more than that, it would be a missed opportunity. The objective of full-fat freeports should be to ensure that the investments made, jobs created, and output produced are an addition to the economy, rather than a diversion. Redirecting economic activity from one region to another is clearly inferior to producing positive-sum growth across the country.”

Ashworth-Hayes concluded that freeports (by which we understand he was talking about the new Investment Zones) could still play a role in generating genuine growth by targeting the UK’s own domestic policy inefficiencies, in particular by:

- Creating a light-touch planning regime to remove a major barrier to growth – acknowledging that the location of businesses attracts demand for housing and services, which in turn create further incentives to make use of the area.

- Providing significant packages of local investment to alleviate concerns about crowding of public services and infrastructure – unofficially ‘buying out’ the objectors with better roads and more GPs – and levelling up in the process.

- Implementing a tax regime within the freeport which is “laser-focused on growth”, in order to justify the cost to the exchequer. (However, we note that reservations were expressed about the efficacy of business rates reduction – the risk being that the rents go up by an amount equivalent to the rates reduction so that only the landowners benefit).

- Establishing a regulatory sandbox – in order words, creating a defined area within which the government can alter regulation to generate evidence of success or failure of policies before implementing them on a national basis.

These ideas are interesting and can be used to support the argument that, for so long as the existing Freeports will encourage growth and not merely lead to a relocation of existing economic activity, so will Investment Zones enhance the existing Freeport locations.

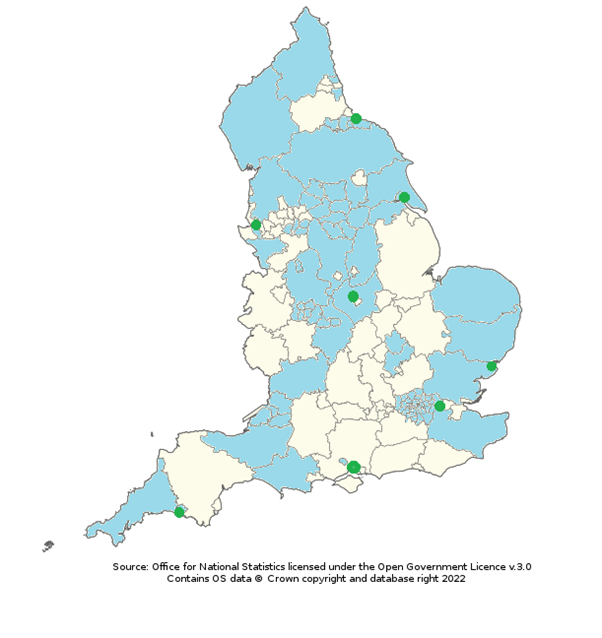

Looking at the situation of the 38 local authorities in discussions over Investment Zones (shown on Map 1, highlighted blue, with the Freeports highlighted green), the geography makes sense: the Freeports are concentrated around sea, rail and airports, and the Investment Zones will be adjacent to them.

In theory, therefore, the Investment Zones should complement Freeports, creating the potential for accelerated development in wider areas to supporting the regional transit hubs. In particular, Investment Zone SDLT relief should support residential development - offering a chance to create residential areas for the human capital drawn to work in the Freeports.

Map 1

For any Freeport site less sure about its prospects of success given the neighbouring Investment Zones and their more generous tax incentives, existing Freeports will be allowed to apply for Investment Zone status. With enhanced and longer lasting tax benefits, this may be an approach for some. Perhaps that depends on progress made to date, given the time limitations of the Freeports tax site benefits.

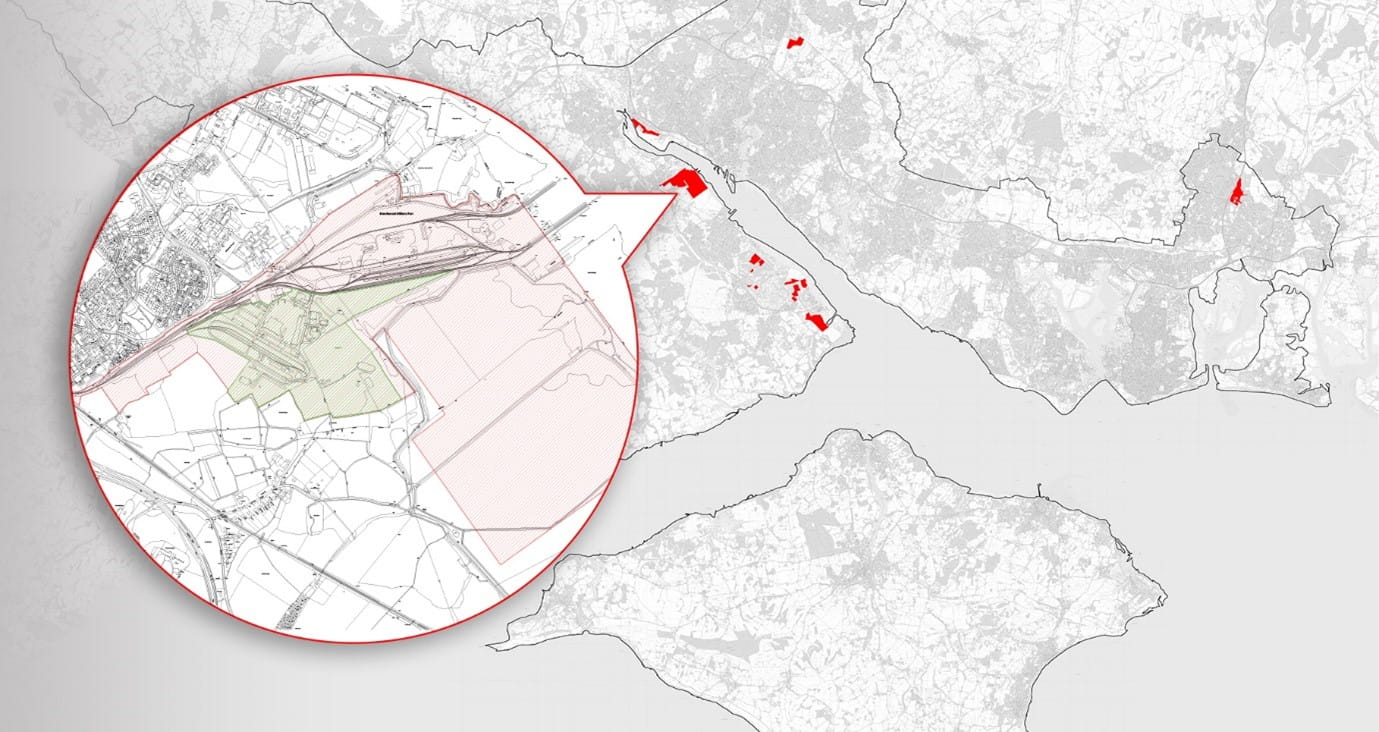

Of course, there are also the customs sites to think about, and perhaps the decision will depend in part on the number of overlapping customs and tax sites within each Freeport. For example, in respect of the Solent Freeport, there are currently six designated tax sites but only one small customs site has been designated. Map 2, which can be seen below, shows that this customs site (in green) sits fully within the Southampton Water Tax Site (Marchwood Port & Strategic Land Reserve) (in red). Another customs site at Portsmouth International Port is due to be designated in the Solent Freeport shortly. However, the Portsmouth customs site will not sit within a tax site as the Marchwood customs site does.

Map 2

Arguably, the government should simply bring the Freeport tax site benefits into line with the Investment Zone tax benefits. It is not really clear why the current differences exist in relation to NICs and enhanced structures and buildings allowances; there would not seem to be a clear policy rationale. The SDLT relief is more understandable (i.e. keeping the focus of Freeports on trade and industry with the Investment Zones more focused on supporting industry with housing stock and services) but the longevity of the reliefs (or rather the lack of it) has always been somewhat surprising, particularly given the time it is taking to get Freeports up and running in practical terms.

What can we learn from Freeport implementation that should shape the development of Investment Zones?

These zones are not created easily.

The Freeports Bidding Prospectus was issued in November 2020, with the first eight freeport locations announced on 3 March 2021 and the legislation providing for the tax reliefs within those sites enacted three months later. The designations did not follow swiftly and arguably there is still not a lot of visible activity.

In order to be designated, the Freeport tax sites needed to satisfy certain criteria. In particular, Freeports are required to satisfy three objectives which were set out in the original bidding prospectus of November 2020, namely: (1) establish national hubs for global trade and investment; (2) promote regeneration and job creation; and (3) create hotbeds of innovation. In addition, Freeport tax sites could only be approved if they are sufficiently underdeveloped, or will become underdeveloped within a reasonably short period of time.

What this meant in practice is that each Freeport location needed to prepare a detailed business case which has been or is being assessed as part of a full tax site assessment process run by HM Treasury. It is assumed that, behind the scenes, significant work has been required to ensure that the tax benefits do not simply translate to higher rents to the lucky landowners within the relevant sites, but will genuinely generate the sought after levels of investment, regeneration and innovation.

We imagine that some sites have created greater challenges than others (for example, relating to existing local infrastructure and natural geographical features) and, as the government will not release the seed capital before those challenges are resolved, the next stage of development is necessarily delayed.

Prospective Investment Zones can learn a lot from Freeports in this respect and, for any Freeport considering a potential neighbouring Investment Zone to be friend not foe, there is scope for knowledge sharing and possibly even a collaborative approach.

Ultimately, however, there is the question of attracting businesses in an increasingly difficult economic climate. Will businesses have the funds to relocate, when the tax incentives are time limited and the areas underdeveloped with no absolute prospect of success? Will businesses ‘shop around’ for the best Investment Zone location and, if so, how will the different Investment Zones compete for investment? How quickly can anything actually change and, given inflationary pressures, can development happen fast enough? Freeports are closer to being able to answer these questions than Investment Zones, but only time will tell.

Will either really get off the ground, and when?

Freeports have been a long time in the making and there still seems to be a long way to go. It might have been good to see continued focus on these areas before announcing the Investment Zones but, given the supportive role Investment Zones can play to Freeports, there is some logic to kickstarting the process for Investment Zones without further delay.

‘If you build it, they will come.’

What seems to be the case, however, is that there is still a great deal of investment interest in Freeports. Whilst it took a year to move from announcement to the earliest tax site designations, it took barely any time to hear of the investment commitments which have already been made. This is unlikely to be due to the tax incentives, especially given how time limited those incentives are, but more likely to be because businesses recognise the opportunity to be a part of the new areas, with links to education and training, cutting edge manufacturing facilities, and support of new technology and the renewable energy sector.

We can expect to hear further announcements in the forthcoming months, with the Investment Zones presenting an opportunity for additional growth. If well executed, the new Investment Zones should be capable of amplifying the ‘ripple effect’ of Freeports, to take the benefits from the immediate Freeport tax and customs sites, to the wider Freeport locations, out into the Investment Zones, and beyond.

Comparison of freeport tax sites and investment zones at a glance

| Benefit | Tax Site within Freeport | Investment Zone |

| The ‘Site’ |

Must be: • in a location clearly delineated within the Freeport’s outer boundary; |

There are no set requirements although sites should: • contribute to the UK’s economic growth; |

| SDLT Relief | Full SDLT relief until 30 September 2026, where the property is to be used for a qualifying commercial activity. Subject to 3-year clawback if land not used in qualifying manner. | Full SDLT relief for land and buildings bought for use or development for commercial purposes, and for purchases of land or buildings for residential developers, potentially over next 10 years. |

| Enhanced Capital Allowances | 100% first year allowance for capital expenditure on plant and machinery from 1 October 2021 until 30 September 2026. The expenditure must be incurred on plant and machinery for the purposes of a trading activity or for other specific activities, mainly in connection with mines, quarries, ironworks, gasworks, waterworks, and certain transport undertakings. The plant and machinery must be for use primarily within a Freeport tax site at the time the expenditure is incurred. | 100% first year allowance for companies’ qualifying expenditure on plant and machinery assets, potentially over next 10 years. |

| Enhanced Structures and Buildings allowance | For businesses acquiring, constructing, or renovating structures and buildings for non-residential use, the enhanced structures and building allowance provides a 10% allowance on straight-line basis rather than the normal 3% per annum. The building or structure must also be brought into non-residential qualifying use before 30 September 2026. | Accelerated relief to allow businesses to reduce their taxable profits by 20% of the cost of qualifying non-residential investment on structures and buildings per year, relieving 100% of their cost of investment over 5 years. Potentially available in respect of expenditure incurred on structures and buildings over next 10 years. |

| Employment tax incentives and NICs rate relief | Enabling employers operating in a Freeport tax site to pay 0% employer NICs on the salaries of any new employee working there, for up to three years per employee on earnings up to a £25,000 per annum. An employee will be deemed to be working in a Freeport tax site if they spend 60% or more of their working hours in that site. The relief is intended to be available for up to 9 years from April 2022, subject to a review no earlier than April 2026; | Zero-rate Employer NICs on salaries of any new employee working in the “tax site” for at least 60% of their time, on earnings up to £50,270 per year, with Employer NICs being charged at the usual rate above this level. |

| Business Rates Relief | 100% relief on certain business premises within Freeport tax sites, from 1 October 2021 and applying for 5 years from the point at which the beneficiary first receives relief before 30 September 2026. | 100% business rates relief on newly occupied and expanded premises. Potentially lasts for up to 10 years. |

| Local Retention of Business Rates | Councils in which Freeport tax sites are located will retain the business rates growth for that area above an agreed baseline for 25 years. | Councils hosting an investment zone will retain the business rates growth for that area above an agreed baseline for 25 years. |

| Planning | Streamlined to aid brownfield site development and increased regulatory flexibility. |

Streamlined consent to grant planning permission to reduce burdensome requirements including: • remove burdensome EU requirements which do not necessarily protect the environment; “The planning system will not stand in the way of investment and development.” |

| Investment incentives | £175 million seed capital fund (up to £25m for each Freeport) to provide matched/part matched public funding for investment in regeneration of sites and qualifying infrastructure. | None announced to date. |

| Innovation | Direct access to relevant regulators through a Freeport Regulation Engagement Network. This will enable an early engagement between businesses and regulators, minimising bureaucracy and uncertainty. |

Additional support to local leaders to ensure their zones can innovate which is to be decided on the requirements for each investment zone but could include: • Wider support for local growth, such as through greater control over local growth funding and, in the case of Mayoral Combined Authorities hosting Investment Zones, a single local growth settlement in the next Spending Review period; |

Disclaimer

This information is for general information purposes only and does not constitute legal advice. It is recommended that specific professional advice is sought before acting on any of the information given. Please contact us for specific advice on your circumstances. © Shoosmiths LLP 2025.